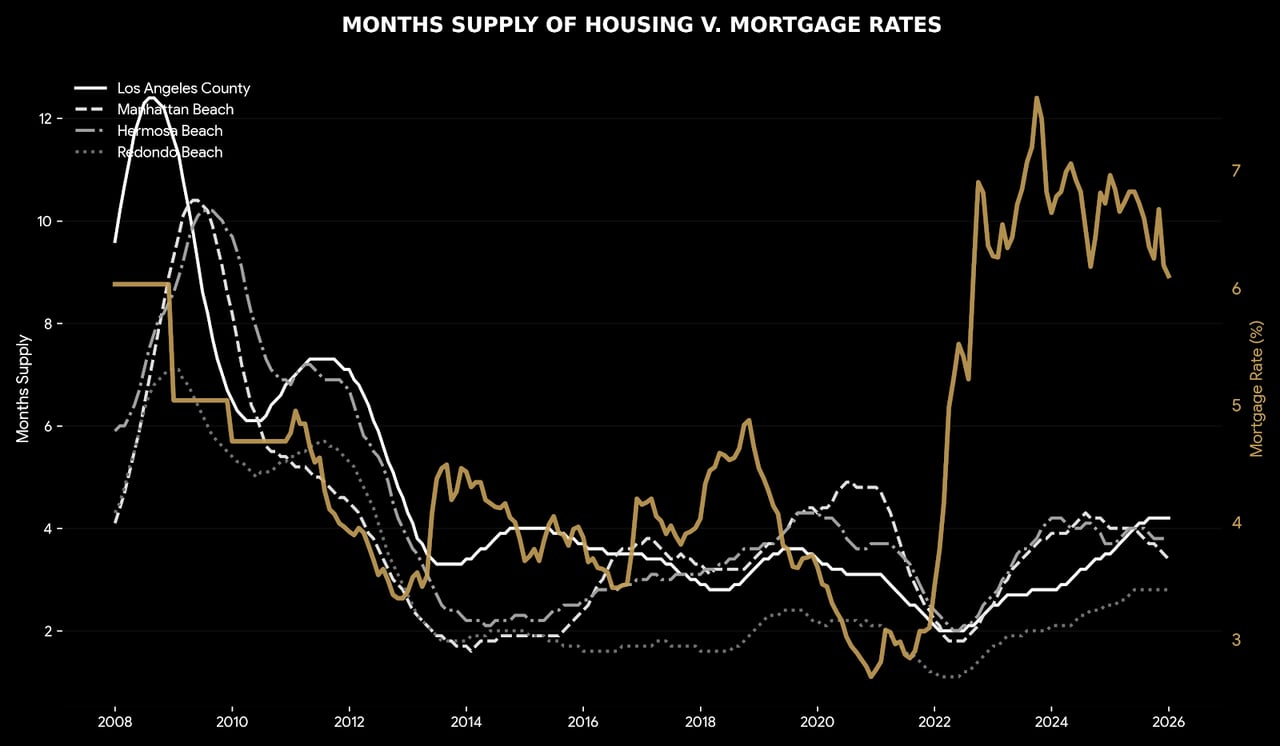

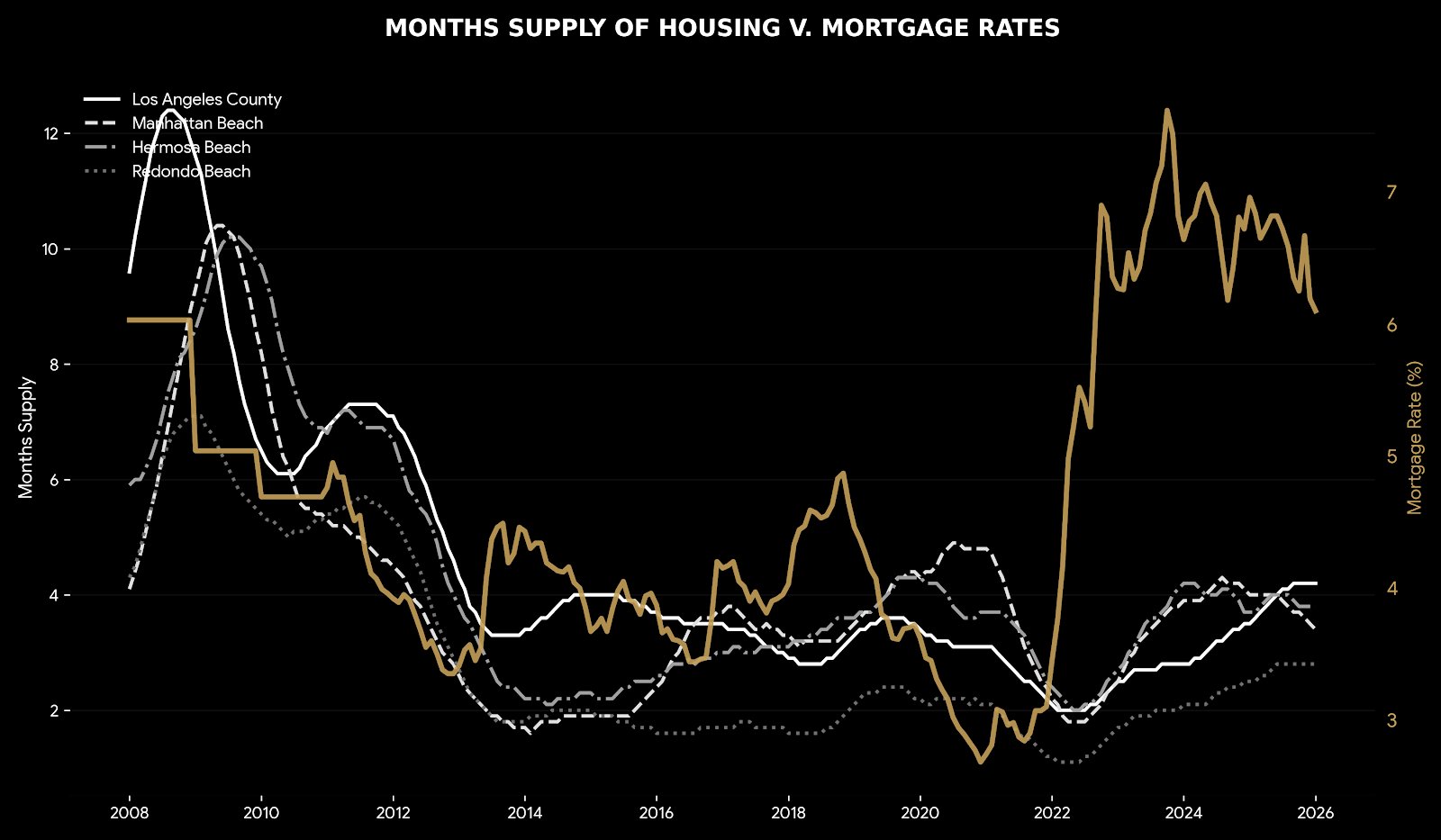

A fascinating dynamic is currently unfolding in the Los Angeles real estate market. As mortgage rates have remained elevated, the "months supply of housing inventory" in the county of Los Angeles has steadily climbed from the hyper-competitive lows of just over one month seen during the pandemic. As of early 2026, the market has reached a more balanced state, with supply sitting at 4.2 months for Los Angeles County. This trend is mirrored in the high-demand beach cities, with Manhattan Beach at 3.4 months, Hermosa Beach at 3.8 months, and Redondo Beach at 2.8 months.

While higher rates have sidelined many potential buyers, it has created a rare window of opportunity. For the first time in years, the market is not defined by scarcity but by choice. This increase in housing supply means less competition, fewer bidding wars, and a greater ability for buyers to negotiate—a market dynamic that has been largely absent from the beach cities for the better part of a decade.

The reason for this market shift is simple economics. As higher mortgage rates increase the monthly cost of a home loan, buyer demand naturally cools off. With fewer buyers actively making offers, homes tend to sit on the market for longer. This causes the total inventory—or "months of supply"—to build up. When this happens, the fundamental power dynamic of the market begins to change. An increased supply of homes for sale forces sellers to compete more directly for the remaining pool of buyers. This new competition is what leads to softening prices, more frequent price reductions, and a greater willingness from sellers to negotiate on terms, putting savvy buyers in a much stronger position.

Let's run the numbers to see why waiting for a slightly better rate could be a costly mistake.

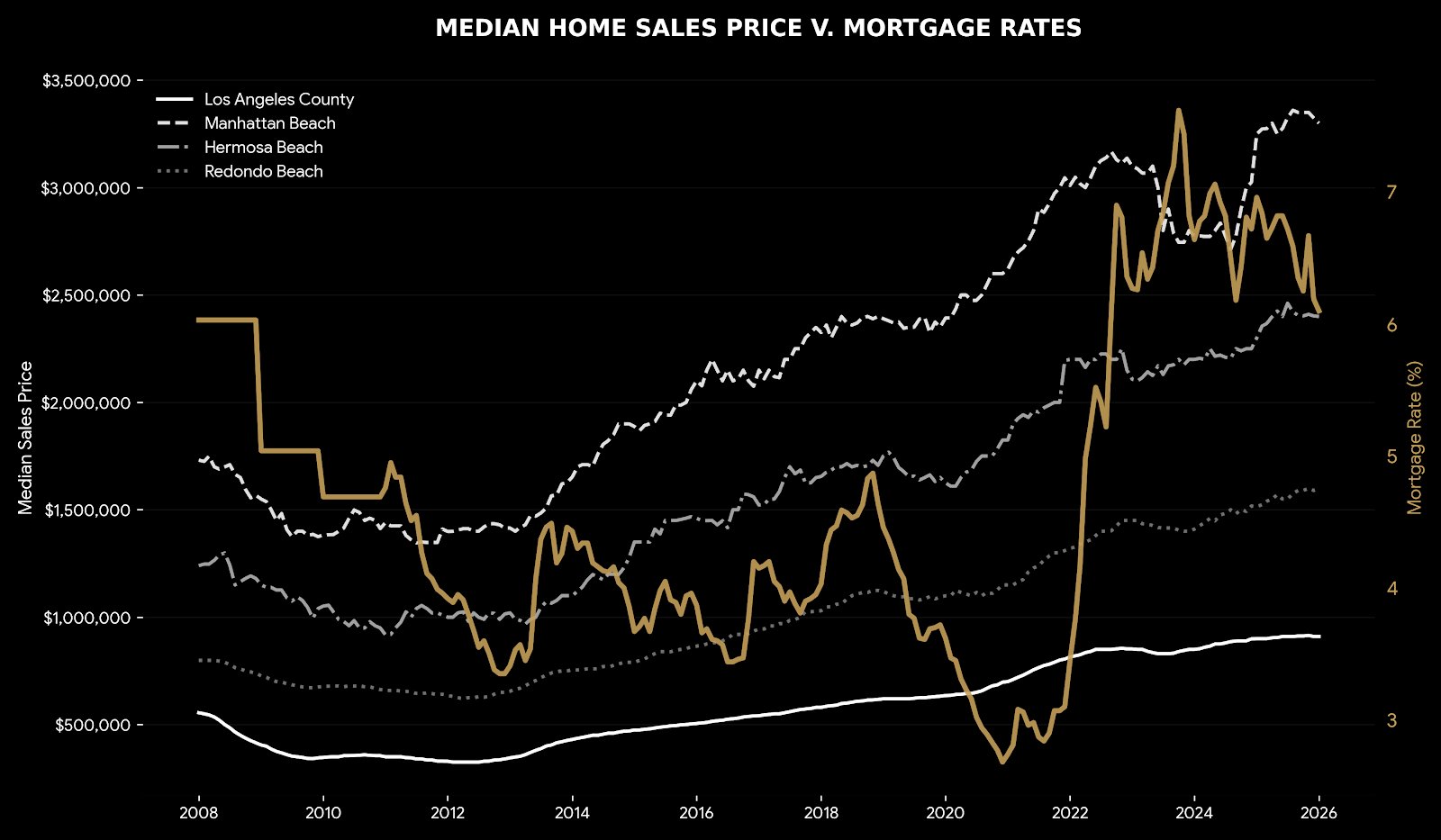

Since 2008, the median sales price in the South Bay Beach cities has increased by an average of about 4.6% per year. Consider a $2 million home with a 20% down payment on a 30-year fixed-rate loan: buying today at a 6.1% interest rate gives you a total monthly payment (P&I + Tax) of roughly $11,779. The property tax portion is based on an assumed rate of 1.25%, which is a market average when factoring in local taxes and assessments. If you wait one year for rates to hopefully drop to 5.75%, that same home, appreciating at the historical average, could now cost approximately $2,092,000. Not only would you need an additional $18,400 for the 20% down payment, but your new total monthly payment would actually be higher at around $11,946 due to the permanently larger property tax bill and higher loan balance.

Beyond the immediate costs, waiting a year means you miss out on the natural appreciation of the home. In this scenario, that’s a lost investment opportunity of $92,000 in potential equity that you would have gained simply by owning the property. The smartest move may be to secure the asset at today's price in a less competitive market and simply refinance the loan when rates eventually come down.

We encourage you to run your own numbers using the Purchase Price & Mortgage Comparison tool below to see how these variables can impact you directly. After all, you can change your interest rate, but you can't change the price you paid.

Purchase Price & Mortgage Comparison Calculator

Compare today's costs vs. a future purchase.

Enter a positive or negative percentage to see impact.

DISCLAIMER: THIS TOOL IS INTENDED FOR INFORMATIONAL AND ILLUSTRATIVE PURPOSES ONLY. THE RESULTS PROVIDED ARE ESTIMATES BASED ON THE INFORMATION YOU PROVIDE, AND ACCURACY IS NOT GUARANTEED. YOU SHOULD NOT RELY SOLELY UPON THE CALCULATIONS IN THIS TOOL AND ARE ADVISED TO CHECK ALL AMOUNTS AND CALCULATIONS PROVIDED. WE ASSUME NO LIABILITY FOR ANY FINANCIAL DECISIONS MADE BASED ON THE INFORMATION PROVIDED BY THIS TOOL.

THE LOAN TERMS YOU MAY RECEIVE MAY BE DIFFERENT FROM THESE ESTIMATES. LOAN QUALIFICATION, INTEREST RATES, AND PAYMENTS ARE SUBJECT TO CHANGE AND DEPEND ON VARIOUS FACTORS INCLUDING YOUR CREDIT HISTORY, FINANCIAL SITUATION, AND PROPERTY DETAILS. PLEASE CONSULT WITH A QUALIFIED MORTGAGE PROFESSIONAL, MORTGAGE BROKER, OR YOUR BANK TO CONFIRM ELIGIBILITY AND FIND OUT WHAT MORTGAGE PRODUCTS ARE AVAILABLE TO YOU.

PROPERTY TAX ESTIMATES ARE BASED ON AN ASSUMED 1.25% ANNUAL RATE AND SHOULD BE CONFIRMED WITH LOCAL AUTHORITIES.